[ad_1]

In keeping with CoStar, there have been 1,264 properties with a mixed whole of 151,129 guestrooms below building in the USA as of November 2024, which represents roughly 2.6 % of the present stock of U.S. lodge rooms. For perspective, the typical month-to-month ratio of rooms below building to whole stock since 2019 is 2.9 %. Additional, the 151,129 rooms below building is the bottom determine since August 2022, which marked the top of the build-out of tasks that started previous to the pandemic. Excessive rates of interest for building loans, mixed with the comparatively excessive prices for building labor and supplies, has suppressed growth exercise.

To investigate present developments in lodge growth exercise, CBRE analyzed building knowledge offered by CoStar. As well as, comparisons had been made to the intentions expressed by lodge buyers in CBRE’s Could 2024 U.S. Resort Investor Intentions Survey. This offered the chance to check the place hoteliers are displaying preferences to construct versus purchase.

What Is Being Constructed?

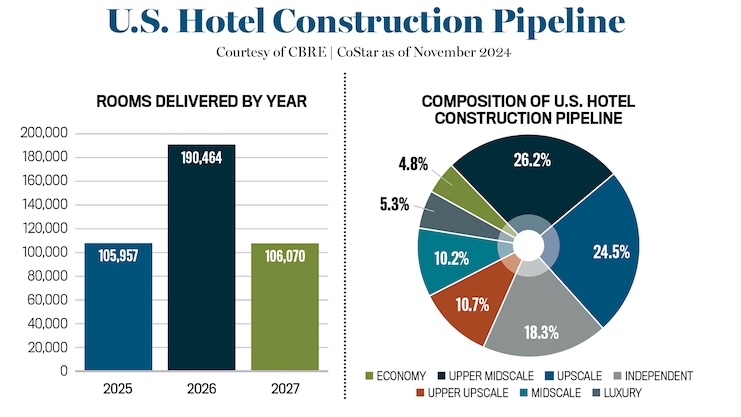

As of November 2024, inns working within the upper-midscale and upscale chain-scale classes dominate the listing of properties below building in the USA. Mixed, these two classes characterize 50.7 % of the whole rooms being constructed. Inns working in these two segments sometimes provide a restricted variety of public areas and facilities, and due to this fact the prices of operation and building are lower than properties working within the luxurious and upper-upscale segments. A lot of the select-service, boutique, way of life, and extended-stay manufacturers which are standard with shoppers are categorized as both upper-midscale or upscale.

Due to their intensive amenities and providers, upper-upscale and luxurious inns are sometimes dearer to construct and require an even bigger footprint. These elements equate to greater building prices, and due to this fact require common each day charges which are difficult to attain in at the moment’s working atmosphere. Higher-upscale inns characterize 10.7 % of the whole rooms below building, whereas luxurious inns comprise simply 5.3 % of the whole.

Roughly 18.3 % of the lodge rooms at present below building are slated for properties that can be operated unbiased of a model. As the prices related to licensing a model improve, lodge house owners are starting to query the worth of a model. Expertise has significantly assisted the advertising and marketing capabilities of inns and enabled them to develop their very own loyalty packages and reservation methods, so for sure varieties of inns which have their very own identification or are in distant locations, affiliation with a model is now not thought of vital.

Traditionally, builders haven’t sought to construct new inns within the economic system and midscale segments. Progress in these two classes has been restricted to older properties which have lived out most of their helpful life and moved down chain-scale classes to function in these two segments. Lately, nevertheless, new moderate-priced extended-stay manufacturers have been created due to the latest success of all these inns. Consequently, the brand new manufacturers have created some curiosity in constructing new midscale and economic system extended-stay properties. Mixed, midscale and economic system tasks make up 15 % of the lodge rooms at present below building in the USA.

Emblematic of the choice for smaller, extra modest-priced properties is the decline within the common dimension of inns within the growth pipeline. The common dimension of a lodge below building dropped from 132 rooms in 2019 to 118 in 2024.

The place and When?

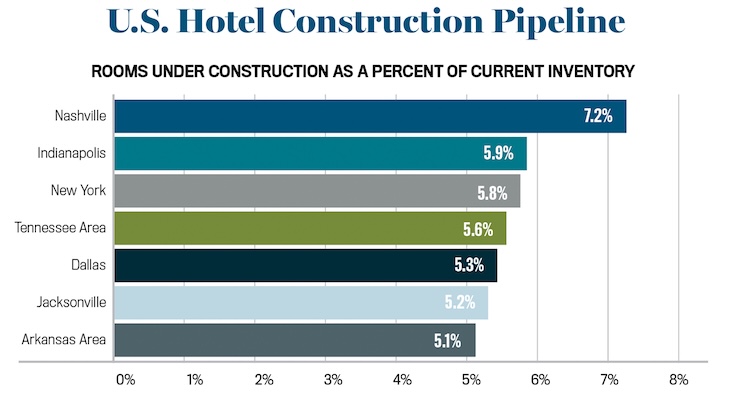

Nashville would be the most impacted market in the USA, as the present building pipeline represents 7.2 % of the market’s current provide. For the previous 15 to twenty years, this ratio in Nashville has remained above the nationwide common, but market efficiency, for probably the most half, has been sustained.

Different markets with building ratios above 5 % are Indianapolis, New York, Tennessee Space, Dallas, Jacksonville, Arkansas Space, and Phoenix. New York stands out as the only real high-density city market throughout the group, as latest restrictions to short-term rental growth, in addition to the conversion of inns to different types of industrial actual property, has attracted lodge builders that may afford to construct a lodge on this market. Most different markets on this group are within the Sunbelt and have comparatively low growth prices and decrease obstacles to entry.

On the opposite finish of the spectrum, lodge rooms below building within the San Francisco/San Mateo space characterize simply .3 % of the present stock. Not solely is that this an costly marketplace for growth, however working efficiency has been, and is predicted to stay, depressed.

A lot of the impression of latest lodge rooms won’t be felt for one more two years. In 2026, 190,464 of the rooms at present below building are scheduled to open. That is higher than the 105,957 rooms scheduled to open in 2025, and the 106,070 rooms slated to open in 2027.

Constructing vs. Shopping for

Every year, CBRE surveys lodge buyers in the USA to find out their present urge for food for lodge funding. Questions within the survey tackle the specified varieties of inns to be bought, favored market areas, and the explanations behind these selections.

In Could 2024, the buyers surveyed by CBRE expressed a bias towards buying inns within the upper-upscale class, which is per the comparatively low new building exercise on this phase. The price of constructing and financing a brand new big-box property is most probably the first affect steering buyers towards pursuing the acquisition of all these inns, versus constructing a brand new lodge.

A distinction between the urge for food to construct or purchase in a market can also be evident when evaluating the present building pipeline to investor intentions. Typically, bigger markets resembling San Francisco, Miami, Boston, and Chicago are most popular targets for purchases, versus new building.

The exception is New York Metropolis, which builders are eyeing for each funding and new building. Nevertheless, latest laws will make new lodge building in New York Metropolis tougher sooner or later after the present tasks within the pipeline open, as the brand new regulation provides lodge unions leverage to dam the event of non-union properties.

Forecasts name for financing and building prices to stay excessive, and due to this fact the impression of latest lodge openings is predicted to be minimal for the following two to 3 years. Nevertheless, hoteliers should perceive the circumstances within the chain-scale phase and market, as funding and growth selections in Nashville are totally different than assessments being made for the San Francisco market.

[ad_2]

Supply hyperlink freeslots dinogame